This content originally appeared on HackerNoon and was authored by Solvency

:::info Authors:

(1) Pietro Saggese, Complexity Science Hub Vienna (CSH);

(2) Esther Segalla, Oesterreichische Nationalbank (OeNB);

(3) Michael Sigmund, Oesterreichische Nationalbank (OeNB);

(4) Burkhard Raunig, Oesterreichische Nationalbank (OeNB);

(5) Felix Zangerl, Austrian Financial Market Authority (FMA);

(6) Bernhard Haslhofer, Complexity Science Hub Vienna (CSH).

:::

Table of Links

- Background and related literature

- VASPs: A Closer Examination

- Measuring VASPs Cryptoasset Holdings

- Closing The Data Gap

- Conclusions, Declaration of Competing Interest, and References

Appendix A. Supplemental material

2. Background and related literature

2.1. Definitions - What is a VASP?

\ While the term VASP has become increasingly common, its precise meaning and the specific activities that fall under this term still need to be clarified. We begin by providing the definition of VASPs according to the FMA (2021), which follows the 5th EU AML directive (EC, 2018) and the Financial Action Task Force guidelines (FATF, 2021). According to this definition, a Virtual Asset, implemented on a distributed ledger technology, is (FMA, 2021, p. VII)

\ […] a digital representation of value that is not issued or guaranteed by a central bank or a public authority, is not necessarily attached to a legally established currency and does not possess a legal status of currency or money, but is accepted by natural or legal persons as a means of exchange and which can be transferred, stored and traded electronically.

\ We note that in the “Market in Crypto Asset Regulation” (MiCA), the term “crypto asset” is used instead of virtual asset. In our context, the two terms can be considered equivalent[4].

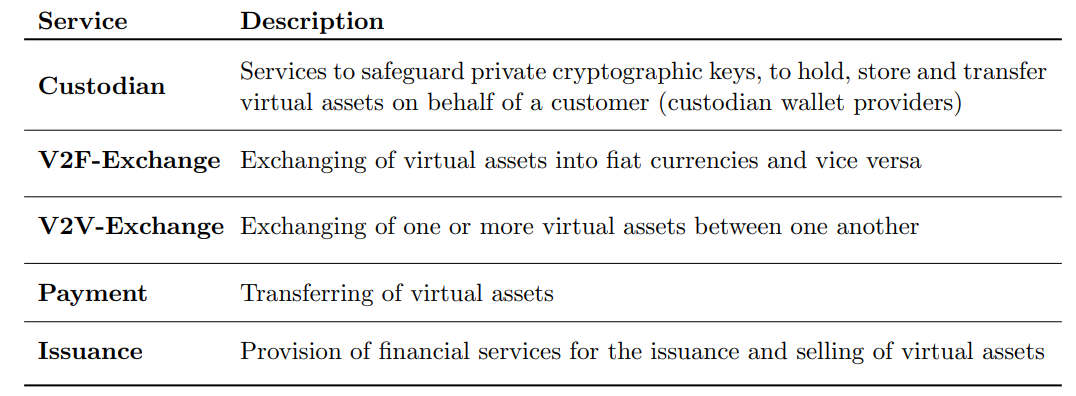

\ Virtual Asset Service Providers are any natural or legal person that, as a business, conducts activities or operations for or on behalf of another natural or legal person. They can offer “[…] one or more services” (FMA, 2021, p. VIII), which we summarize in Table 1.

\

\ VASPs lie at the interface of the traditional and the crypto financial ecosystems. The former encompasses financial activity with fiat currencies, i.e., legal tender money, and fiat assets, i.e., assets denominated in fiat currencies (similarly to cryptoassets being assets denominated in a cryptocurrency). It can rely on commercial banks and other traditional financial intermediaries. The latter entails financial activity executed on Distributed Ledger Technologies (DLTs) like the Bitcoin and Ethereum blockchains, and with cryptoassets such as bitcoin, ether, and the stablecoins tether (USDT), USD coin (USDC), or DAI.

\ On the off-chain side, VASPs and customers interacting with them have strong identities; that is, the former need to register with regulatory bodies and the latter undergo identification processes such as KYC and AML5 compliance. On the on-chain side, activities involve weak identities (M¨oser et al., 2013; Ford & B¨ohme, 2019): transactions, enabled by cryptographic keys, occur among pseudonymous counterparts, and the same entity can control multiple addresses.

\ We also note that VASPs differ from decentralized finance (DeFi) actors. This term indicates an emerging financial ecosystem built on DLTs that is non-custodial and does not require a central organization to operate (Auer et al., 2023). VASPs are instead centralized intermediaries that provide interfaces to exchange cryptoassets via conventional IT systems, and transactions are not necessarily recorded on DLTs but at times are rather stored in private ledgers (Aramonte et al., 2021; Auer et al., 2022a).

\ 2.2. Proof of Solvency

\ A company is solvent if the total amount of assets held in custody is larger than the total amount of liabilities, whereby the difference is equity. Substantial documentation exists regarding incidents and exchange closures of VASPs (Moore et al., 2018), including recent events such as FTX’s bankruptcy filing. To increase transparency and foster trust, several VASPs have recently disclosed lists of cryptoasset wallet addresses as a proof of reserve, i.e., proof that they hold a given amount of assets. However, such an approach alone does not constitute a valid proof of solvency because it does not guarantee that VASPs have the financial resources to meet their current and future obligations[5]. First, a proof of deposits, i.e., a verification of the customers’ deposit amount, is needed as well (Buterin, 2022). Second, in addition to revealing the existence of an address, it is necessary to prove control over the corresponding private key. Third, even this might not be sufficient, as colluding actors could lend each other cryptoassets to conduct one-time proof of reserves.[6]

\ Data from the commercial register contains both information on the asset and liability side of VASPs balance sheets, and the fiat assets are audited according to generally accepted accounting principles. Therefore, in our context, it is sufficient to verify that the asset side is consistent with the cryptoasset holdings of a VASP to prove its solvency.

\ 2.3. Traditional financial intermediaries

\ VASPs allow customers to deposit and exchange assets, and can provide consulting and portfolio management services for their customers, often holding funds on behalf of their customers (Anderson et al., 2019). Therefore, they share several characteristics with traditional financial intermediaries. Here we describe the ones that are most important in our context and their main economic functions. A comprehensive description of traditional financial intermediaries can be found in Howells & Bain (2008) and Cecchetti & Schoenholtz (2014).

\ The two primary financial intermediary categories are deposit-taking institutions (DTIs) like banks and non-deposit-taking institutions (NDTIs) such as brokerage firms, mutual funds, and hedge funds. Other DTIs include building societies (UK), savings and loan societies (US), and mutual and cooperative banks (DE, FR). The main difference is that DTIs issue loans and use their liabilities as official money (Howells & Bain, 2008). Consequently, an increase in DTI business ultimately increases the money supply in an economy.

\ Banks, by far the most important DTIs, pool small savings to make large loans. They also provide liquid deposit accounts, access to the payment system, and screen and monitor borrowers. Among NDTIs, brokerage firms facilitate access to trading in financial instruments. They offer custody and accounting services for customer investments and are additionally involved in the clearing and settlement of trades. Mutual funds, including exchange-traded funds (ETFs), sell shares to customers and invest in a diverse range of assets offering access to large, diversified portfolios. Hedge funds operate as financial partnerships, often requiring accredited or highnet-worth investors. They pool savings to earn returns through actively managed investment strategies, including derivatives, arbitrage, and short sales.

\ 2.4. Literature

\ The academic literature on VASPs is vast and primarily focuses on cryptoasset exchanges, highlighting the central role they have in the crypto ecosystem (Makarov & Schoar, 2021; Lischke & Fabian, 2016). Recent studies show that most of the trading on cryptoasset markets happens off-chain on CEXs (Auer et al., 2022b; Brauneis et al., 2019); according to Makarov & Schoar (2021), 75% of the bitcoin transactions involve exchanges or exchange-like service providers. CEXs play a major role also as they facilitate price discovery (Brandvold et al., 2015). Scholars exploited price time series from the largest exchanges to investigate the price formation dynamics (Kristoufek, 2015; Katsiampa, 2017; Li & Wang, 2017) and estimate the fundamental value of cryptoassets (Cheah & Fry, 2015; Kristoufek, 2019). Other studies used instead exchange-based data to investigate topics such as market (in)efficiency (Urquhart, 2016; Kristoufek, 2018), the behavior of bitcoin as a currency or asset (Glaser et al., 2014; Yermack, 2015), the effects of cross-listing on returns (Benedetti & Nikbakht, 2021), as well as arbitrage, both across exchanges (Makarov & Schoar, 2020) and within one exchange alone (Saggese et al., 2023). Exchange data were also used to study market microstructure aspects, such as price jumps (Scaillet et al., 2020), or market liquidity (Brauneis et al., 2022). Another relevant strand of literature investigates risks associated with CEXs such as price manipulation (Gandal et al., 2018), susceptibility to attacks (Feder et al., 2017), wash trading (Chen et al., 2022) and data fabrication (Cong et al., 2022).

\ Previous studies have provided taxonomies or categorizations of crypto financial intermediaries (Kazan et al., 2015; Blandin et al., 2020) and compared them to traditional ones (Aramonte et al., 2021). In Fang et al. (2022), the authors define cryptoasset trading and survey the related works. Our work differs in that we base our categorization of virtual asset service providers on the legal definition of the Austrian Financial Market Authority. Then, we identify the financial functions that VASPs offer and provide an overview of the different types of VASPs.

\ Close to our work, Decker et al. (2015) and Dagher et al. (2015) implemented a softwarebased solution to automate the audit of centralized Bitcoin cryptoasset exchanges. Other works focused instead on proof of reserves for less relevant DLTs (Dutta & Vijayakumaran, 2019a,b; Dutta et al., 2021). Our work differs as it is based on an empirical approach that cross-references multiple different sources of information (cryptoasset wallets, balance sheet data from the commercial register, and information from supervisory entities), and because it focuses on the two most relevant blockchains (Bitcoin and Ethereum), but can be extended to others.

\

:::info This paper is available on arxiv under CC BY 4.0 DEED license.

:::

[4] MiCA also refers to crypto asset service providers (CASPs), rather than to VASPs. For the purpose of this work, VASPs and CASPs can be considered as synonymous as well.

\ [5] proof of reserves and proof of solvency are terms adopted in jargon. More technically, the latter is the capital cushion to fulfill liabilities and obligations against customers, i.e., the capital requirements. Proof of reserves were collected by projects such as DefiLLama, which gathered several CEX wallet addresses: https://bit.ly/3KpdnHT.

\ [6] See e.g., https://bit.ly/3XXBlgP and https://bit.ly/3DjaJiq.

This content originally appeared on HackerNoon and was authored by Solvency

Solvency | Sciencx (2024-06-19T14:00:17+00:00) Assessing VASP Solvency For Cryptoassets: Background and related literature. Retrieved from https://www.scien.cx/2024/06/19/assessing-vasp-solvency-for-cryptoassets-background-and-related-literature/

Please log in to upload a file.

There are no updates yet.

Click the Upload button above to add an update.