This content originally appeared on HackerNoon and was authored by Bhavdeep Sethi

\ \ In finance, investors have a wide range of options to consider when looking to build their portfolios. Mutual funds serve as one of the more traditional ways to purchase a diversified basket of securities. Exchange-traded funds (ETFs) offer savvy stockholders tax efficiency and cost-effective expense ratios. However, for those looking to exercise the greatest control, direct indexing is emerging as the optimal investment instrument. This approach allows investors to directly own the individual securities within an index, providing even greater tax-loss harvesting opportunities and personalization while retaining the benefits of an ETF.

\

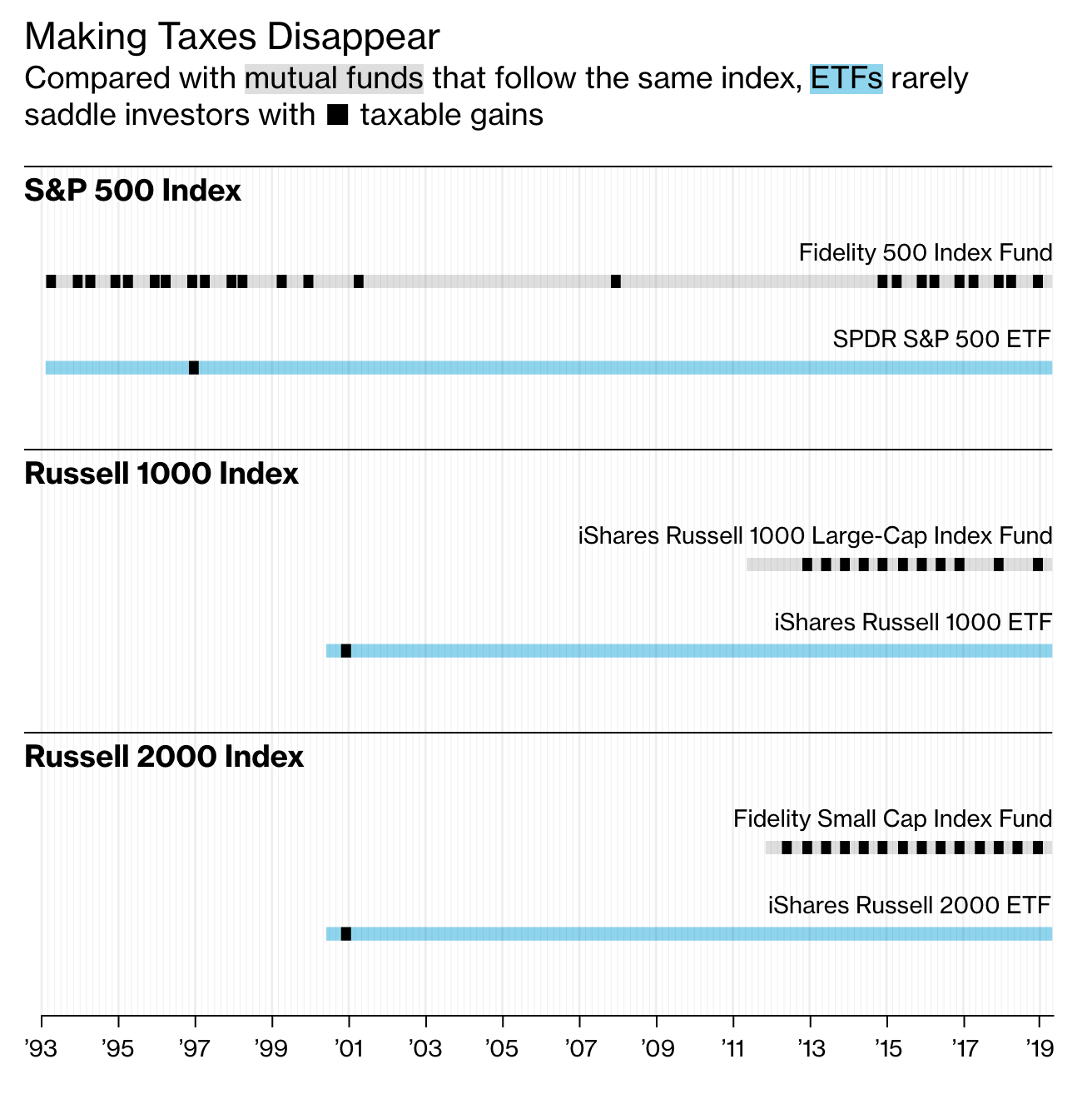

Understanding the ETF tax advantage

To fully grasp the advantages of direct indexing, it's essential to understand the tax advantages of ETFs compared to mutual funds. While both products pass on capital gains distributions to their owners, this rarely occurs for ETFs due to their use of in-kind creation and redemption. This process, which involves exchanging securities directly rather than selling them, helps minimize taxable events.

Source: Bloomberg

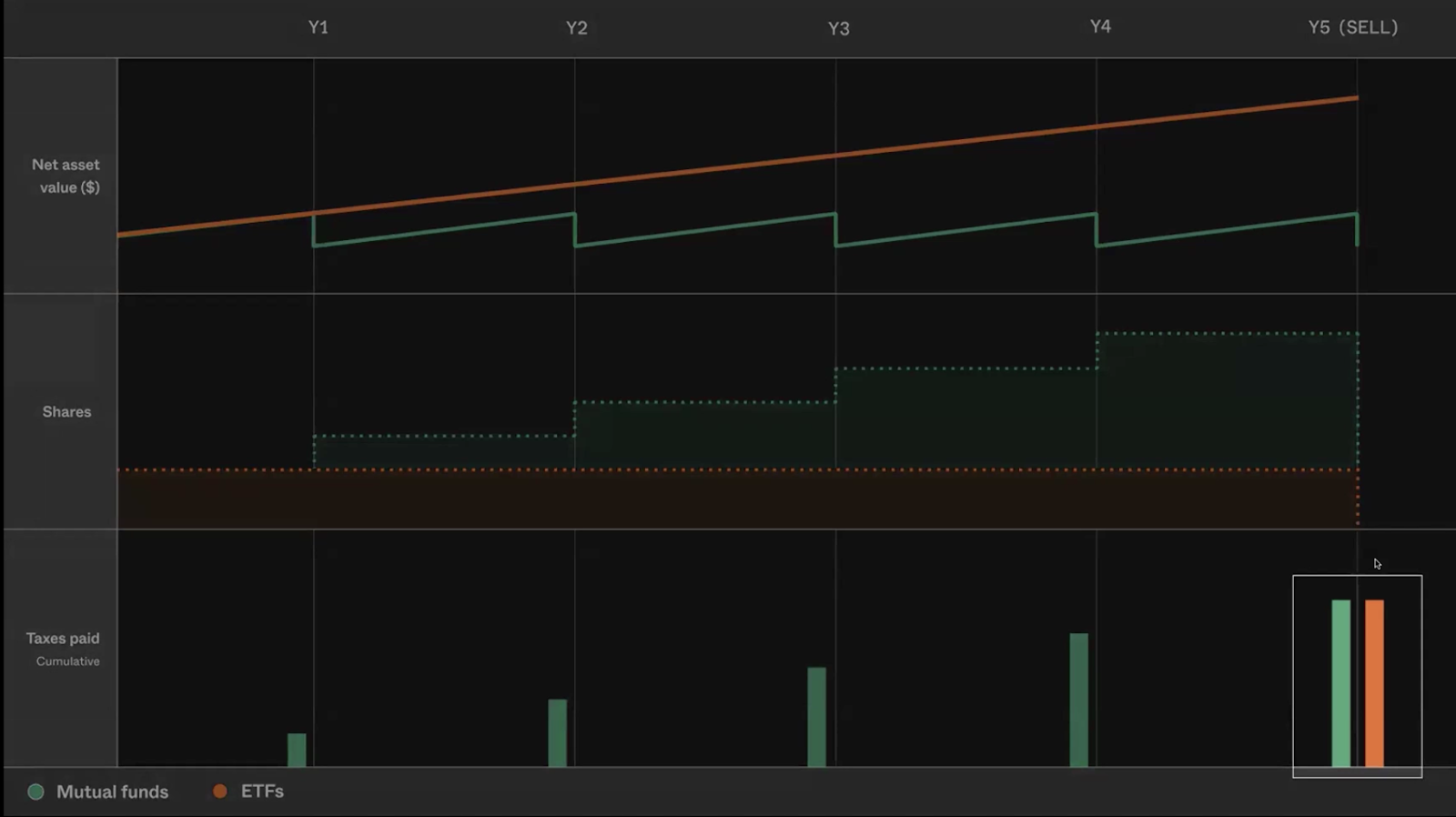

\ Illustrating this with a simplified example, imagine you purchase $100 worth of a mutual fund at the beginning of the year. The fund appreciates 10% by the end of the year, bringing your investment's value to $110, resulting in a $10 capital gain. As mutual funds distribute these gains to their investors, you would pay $3 in taxes on this gain (assuming a 30% tax rate), and the remaining $7 is reinvested to purchase additional shares. Each year, this cycle repeats: gains are distributed, taxes are paid, and additional shares are acquired; in five years' time, you have consistently paid taxes on your gains.

In contrast, consider an ETF, which does not pass down capital gains distributions; consequently, your number of shares remains the same. At the end of the five-year period, if you decide to sell the ETF, you would then realize a capital gain and pay the associated taxes. The total amount paid over the five years is equivalent in both scenarios. The key difference lies in the timing: With a mutual fund, you pay taxes annually on the distributed gains, whereas with an ETF, you defer the payment until you sell, potentially benefiting from the deferred tax advantage. Goldman Sachs projects this value to be 4.4% over a period of 10 years, which can grow further according to your investment window—no paltry sum in the world of compounding returns.

\ Beyond the cumulative gains, ETFs offer another long-term benefit: When an ETF is inherited, its cost basis is adjusted to the fair market value on the date of the owner's death. This step-up in basis means your beneficiaries will owe less in taxes compared to inheriting mutual fund shares, which do not receive such favorable tax treatment.

\ ETFs allow your investments to grow sustainably, providing strategic advantages for financial planning across a much longer investment window. To take your portfolio optimization a step further, we turn to direct indexing.

\

Taking control with direct indexing

Consider a popular ETF, such as SPY, which tracks the S&P 500. With direct indexing, you purchase the underlying constituents of the index in proportion to the target weight used by the ETF. When any individual constituent dips below its cost basis, you sell it to harvest losses and buy an alternate security for thirty days. After this period, you can buy back into the original position. This allows you to accumulate granular, timely losses while continuing to track the index closely, all of which can be claimed as tax deductions.

A more concrete example* with a single security: An investor purchases TSLA for $20,000, holding on to it while it's below the cost basis, and eventually selling for $30,000, for $10,000 in capital gains.

In a tax loss harvesting scenario, the investor takes advantage of the drop below cost basis, harvesting the loss, and temporarily buys a correlated basket of stocks. The investor then quickly moves back to TSLA and, as in the first scenario, sells at $30,000 for a gain of $16,000. While the net capital gain is still $10,000, as in the first example, the $6,000 in losses can now be used to offset other gains in or outside their portfolio, thereby reducing their overall tax bill.

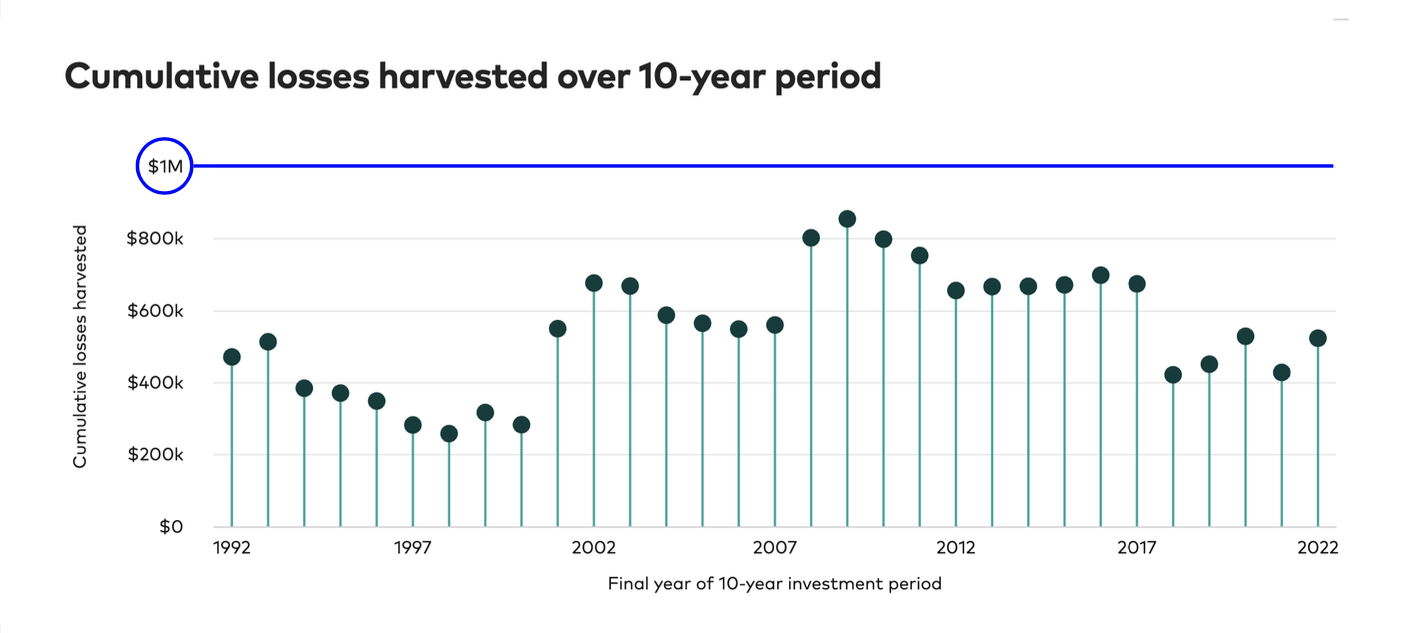

\ Modern direct indexing strategies eliminate the need to monitor and track each security manually, performing these complex and time-sensitive actions programmatically across all constituents. Over time, this has been shown to generate 40% of the initial deposit in capital losses over a period of 10 years, with most of the losses front-loaded and diminishing over time.

Vanguard simulations for a $1M portfolio, over different 10-year periods, show similar results.

\ Accounting for cumulative tax losses

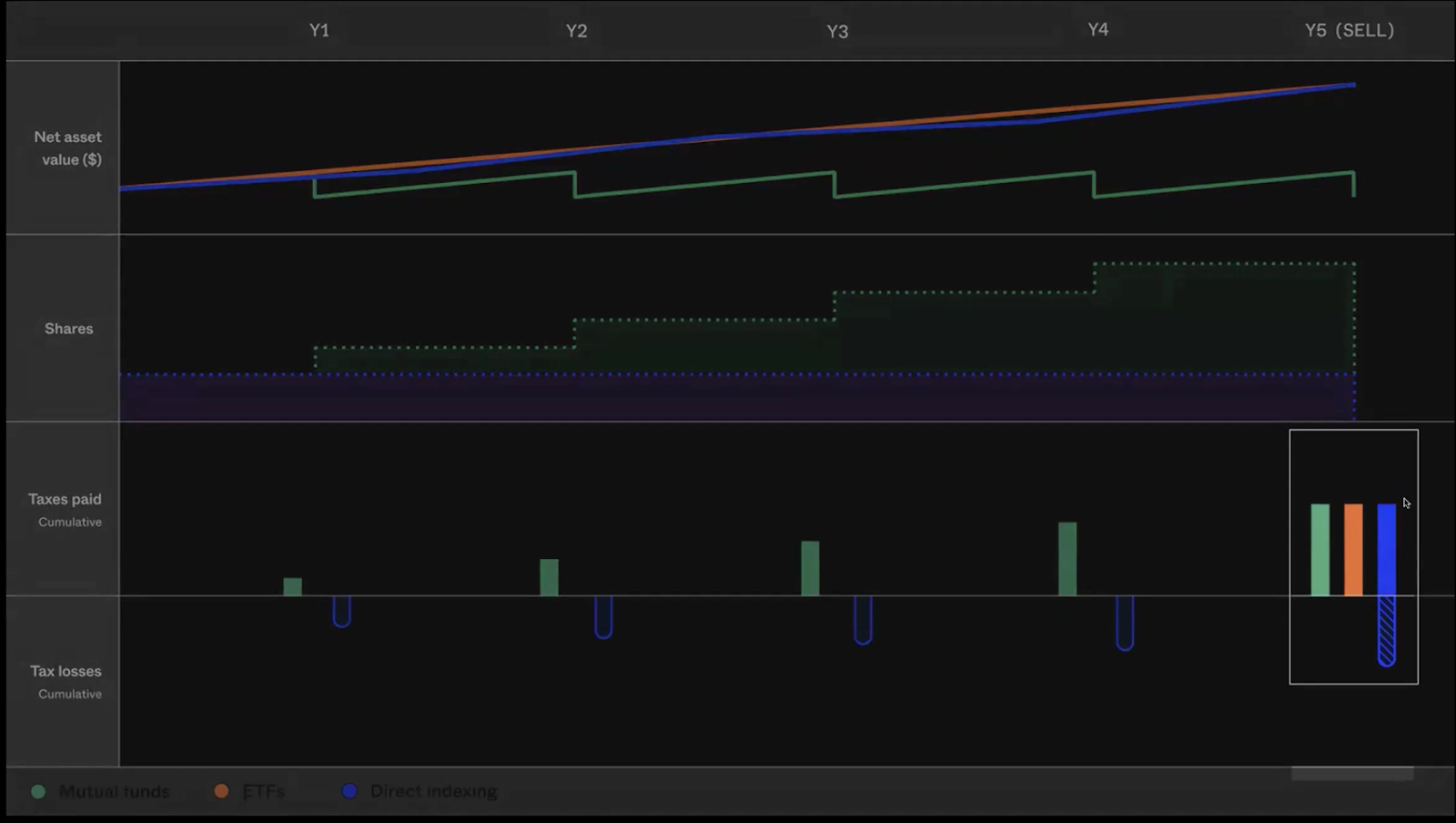

We see that direct indexing is similar to an ETF in terms of asset value and the number of shares. In the above five-year projection, by reducing your cost basis in direct indexing, you will have higher capital gains when liquidating. However, your accumulated losses offset those gains, ensuring the net tax paid is identical to owning either a mutual fund or ETF.

\ The appeal of direct indexing, then, lies in taking advantage of capital losses early and creating flexibility in your tax bill. There are no limits to how much capital gains can be offset in your portfolio, and unused capital losses carry over each year. These losses can be leveraged to diversify out of over-concentrated stock positions, which might incur capital gains, offset gains from selling real estate, exit an angel investment, or mitigate major capital gains events like acquisitions and IPOs.

\ In years with fewer gains, you can claim $3,000 of deductions against ordinary income. Reinvesting these tax savings back into the market enables compounding gains that would otherwise be unavailable with ETFs. A Vanguard study quantifies the benefits for direct indexing as a tax alpha of 1.36% to 3.10%, on top of market returns.

\

The growing wave of direct indexing

\ Despite being a decades-old investing product, direct indexing and its costs once made it exclusive to large investors and family offices. Why is it gaining in popularity today?

\ · Fractional shares have lowered the barrier to entry, allowing for a greater range of funding strategies.

· Zero-commission trading has introduced more frequent loss harvesting opportunities.

· Lower compute costs have given rise to more advanced optimizations for strategies that leverage automation.

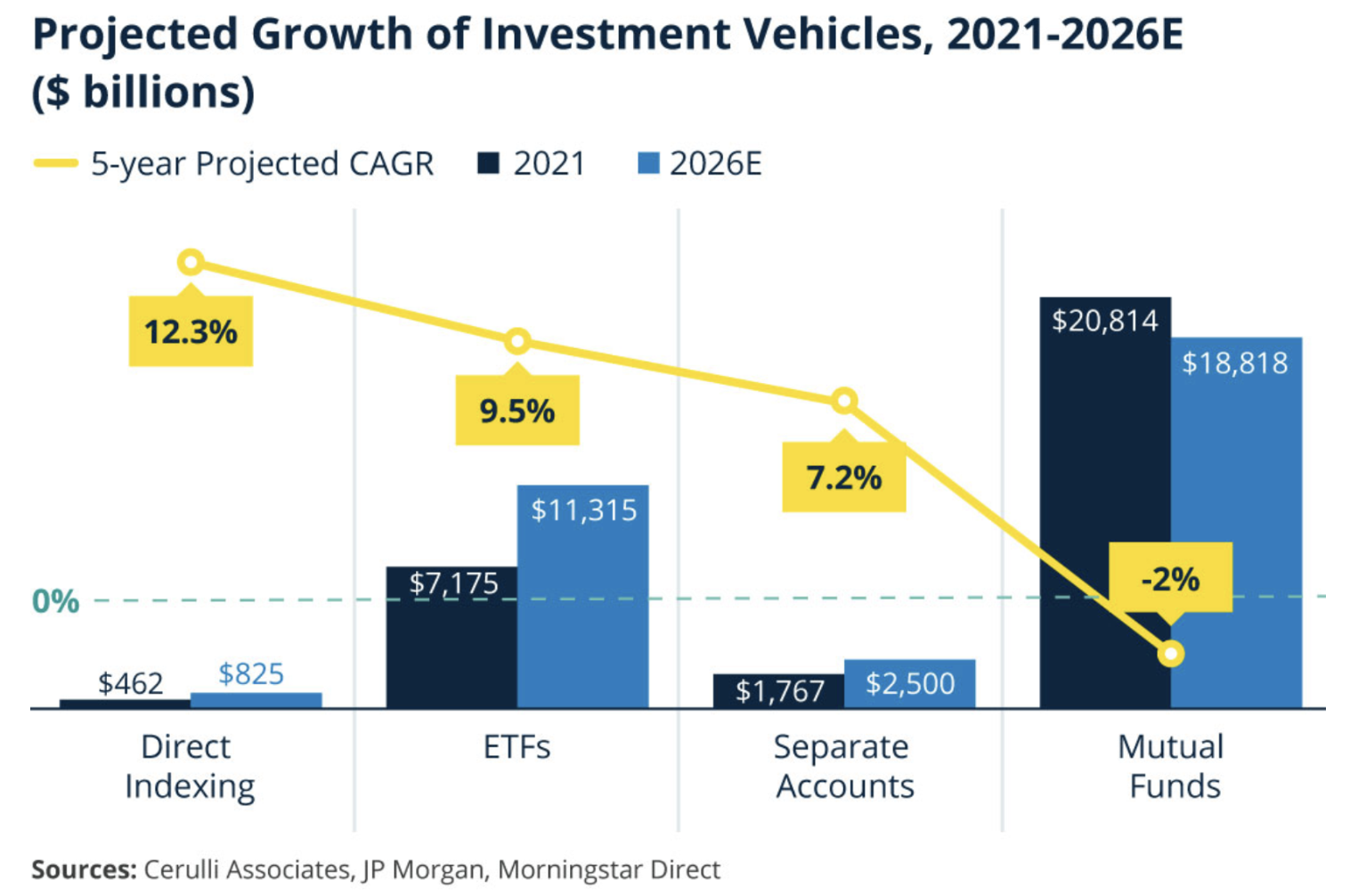

Direct indexing is outpacing both ETFs and mutual funds, with assets predicted to exceed $800 billion by 2026. In a market fraught with uncertainty, stockholders would do well to read the sea change: Direct indexing is becoming the leading opportunity for those wanting the greatest control of their investments.

\ Note: This is simply an example to explain how tax loss harvesting works. Stocks don’t have to be sold on year 3 to do this.

\

:::info Disclosure: I work for Frec, who offers a direct indexing product to retail customers.

:::

\n

This content originally appeared on HackerNoon and was authored by Bhavdeep Sethi

Bhavdeep Sethi | Sciencx (2024-09-27T12:51:58+00:00) The Next Frontier of Passive investing. Retrieved from https://www.scien.cx/2024/09/27/the-next-frontier-of-passive-investing/

Please log in to upload a file.

There are no updates yet.

Click the Upload button above to add an update.