This content originally appeared on HackerNoon and was authored by Keynesian Technology

:::info Andrea Renzetti, Department of Economics, Alma Mater Studiorium Universit`a di Bologna, Piazza Scaravilli 2, 40126 Bologna, Italy.

:::

Table of Links

Forecasting with the TC-TVP-VAR

Response analysis at the ZLB with the TC-TVP-VAR

3 Forecasting with the TC-TVP-VAR

In this section I consider the problem of forecasting the rate of growth of GDP, the inflation rate and the Fed Fund rate using a trivariate TVP-VAR model. In the specific, I estimate a trivariate TVP-VAR for the US economy using data from 1970 up to 2019 and I compare the forecast accuracy of a standard TVP-VAR model to the forecasts from a TC-TVP-VAR.

3.1 Small scale New Keynesian model for the US economy

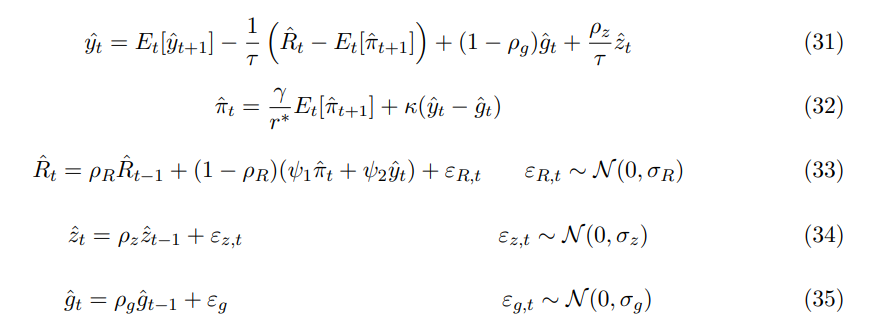

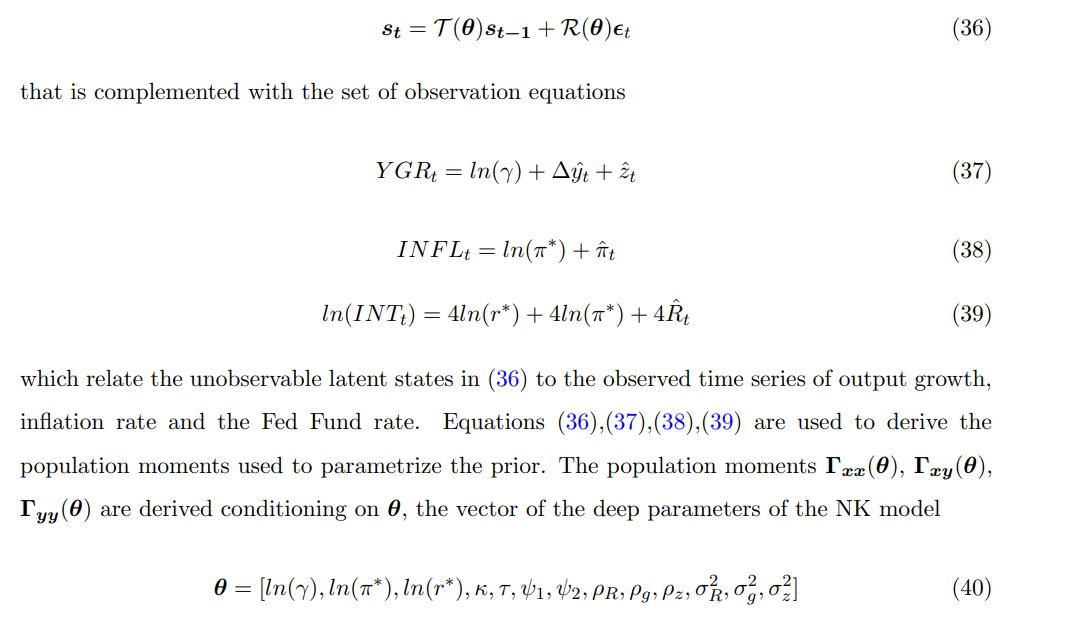

In the TC-TVP-VAR I exploit the New Keynesian model in Del Negro et al. (2004) to parametrize the theory coherent prior. The conceptual framework commonly denoted as the 3-equation New Keynesian model constitutes the nucleus of Michael Woodford’s book “Interest and Prices” (Woodford 2003) and underpins most of modern monetary macroeconomics models.[21] More specifically, the structural model is composed by an IS curve (31), a New Keynesian Phillips curve (32), a monetary policy rule (33) and two equations that describe the dynamics for the log-deviation from the steady state of technological process (34) and government spending (35), namely

\

\ The population moments needed to parametrize the prior are derived from the state-space representation of the New Keynesian model obtained by solving the system of non-linear rational expectation equations. In particular, the non-linear rational expectation equations are solved using the method based on matrix eigenvalue decomposition by Sims (2002) leading to a solution which has the form

\

3.2 Forecast comparison

Table 1 shows the comparison of the forecasts from a standard TVP-VAR model and the TCTVP-VAR model. The forecasting exercise is designed such that I compute the recursive one quarter, two quarters, and one year ahead forecasts starting from 1985-Q1 up to 2019-Q4.22 To compare relative point forecast accuracy, in the table I report the Root Mean Squared Error (RMSE) while for evaluating density forecast accuracy I report the average Cumulative Ranked Probability Scores (CRPS). In the table I also include the results concerning the forecasts from a constant parameters VAR with flat prior and a constant parameters Bayesian VAR (BVAR) with Minnesota type of prior.23 Overall, the TC-TVP-VAR provides the most accurate point and density forecasts for both output growth and inflation rate, outperforming the standard TVP-VAR model at all the horizons considered. For forecasting output growth, the standard TVP-VAR performs poorly relative to the TC-TVP-VAR, but also to the constant parameters BVAR with Minnesota prior, suggesting that the model tends to fit some noise in the time series of output growth. In line with the previous forecasting literature, allowing for time variation of the parameters of the VAR is important for obtaining accurate forecasts of the inflation rate, as the standard TVP-VAR outperforms both the VAR with flat prior and the BVAR with the Minnesota prior. However, economic shrinkage is helpful to obtain more reliable point and density forecasts when modelling the time variation of the coefficients. Indeed the TC-TVP-VAR outperforms the standard TVP-VAR at all the horizons. As a caveat, the standard Minnesota prior centering the autoregressive coefficients on a random walk process outperforms the other competitors, including the TC-TVP-VAR, for forecasting the Fed Fund Rate. This result is consistent with the results of the forecasting exercise in Del Negro et al. (2004) which use the same small scale NK model to parametrize a prior for a constant parameters VAR.

\

:::info This paper is available on arxiv under CC 4.0 license.

:::

\

[21.] See Del Negro et al. (2004) for the more in depth details on the New Keynesian Model.

\ [22.] Details on the data can be found in the appendix A.2.1

\ [23.] Appendix A.2.2 the reports details on the competing forecasting models

This content originally appeared on HackerNoon and was authored by Keynesian Technology

Keynesian Technology | Sciencx (2024-09-04T17:00:18+00:00) Theory Coherent Shrinkage of Time Varying Parameters in VARs: Forecasting with the TC-TVP-VAR. Retrieved from https://www.scien.cx/2024/09/04/theory-coherent-shrinkage-of-time-varying-parameters-in-vars-forecasting-with-the-tc-tvp-var/

Please log in to upload a file.

There are no updates yet.

Click the Upload button above to add an update.