This content originally appeared on Level Up Coding - Medium and was authored by Marc Clotet

Understanding the Differences Between Indirect, Direct and Hybrid CBDCs

Deeming the far-reaching recent enthusiasm in the crypto-world, it is of no surprise that Central Banks would not like to be left behind in the race for new disruptive payment instruments which can shape the banking industry.

The Bank for International Settlements (BIS) has been conducting interesting research on Central-Bank Issued digital currencies and worldwide Central Banks are beginning to welcome new initiatives regarding CBDCs. According to a fresh survey involving 63 Central Banks, a third of CBs have perceived CDBCs as a possible medium- to long-term project.

Notably, the People’s of China’s Digital Currency Research Institute led various trials of a wide use of an eCNY and is proving to be reasonably successful. However, is China trying to get ahead in the global financial order or is the sole purpose of a digital Yuan research-oriented, aiming at more ambitious long-term outcomes?

The reality is that China’s regulators and policymakers must deal with huge pressures from the private financial sector which is becoming slightly more important in terms of the volume of electronic payments share in the Asian country. Alipay and WeChat Pay, China’s ‘Big Two’ privately owned financial services providers, are enlarging their electronic operations day-by-day. Moreover, the West may also think about China seeking an alternative to the U.S. dollar, which is world’s par excellence fiat currency since the majority of CBs’ reserves are dominated in dollars, and to SWIFT, whereby unleashing the old continent from an era predominated by western-capitalist rules.

Although a digital Yuan is not the main purpose of this brief, it is important to highlight China’s incredible advances in the electronic payments industry, so as to understand the similarities that a possible near future issuance of a ‘’retail’’ CBDC may entail for Western Europe and the United States. In the. remaining of this article, I explain the main three types of a CBDC concerning its design.

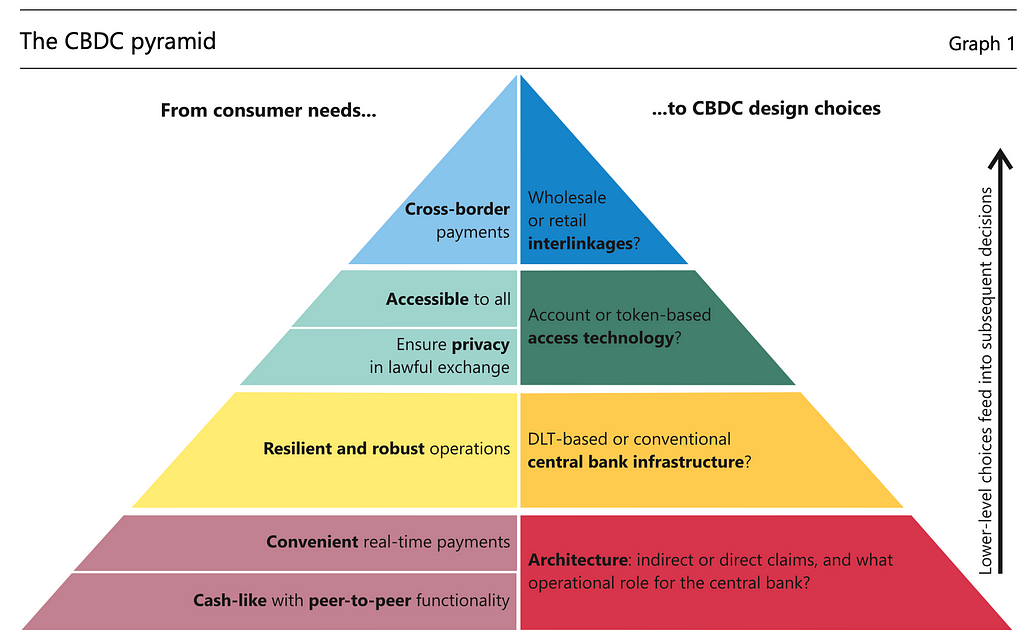

Design Choices: the ‘CBDC Pyramid’

Technological design considerations of a CBDC is related to households’ (consumers) needs and prefrences when making a decision on which payment instrument to use. Figure I depicts this relationship between consumer needs (RHS) and the optimal design choice of CBDCs (LHS). We must bear in mind that a “retail’’ CBDC would merely embody a sort of ‘cash-like’ claim on the CB, whereby the CB would become the only issuer and, hence, the ultimate controller of such a fiat money. Notwithstanding, Central Banks may enable the entry of third-parties which might secure households’ heterogenous preferences for ‘anonymity’, therefore, offering CBs partial anonymity in the transactions.

The architecture of a CDBC is also of great importance; the choice between a distributed ledger techonology (DLT) or a centrally controlled infrastructure may depend on each CB own policy (Auer R., Böhme R., 2020).

‘Is the CBDC a direct claim on the CB or is the claim indirect, via payment intermediaries? What is the operational role of the CB and of private sector intermediaries in day-to-day payments?’

Since CBDCs core principles rely on the resemblance of cash and its convenience of use — as indicated by the first and second bottom layers from Figure I, the whole operational architecture will depend on these two needs.

However, the design choice will be shaped by two main questions raised in Auer et al.; ‘Is the CBDC a direct claim on the CB or is the claim indirect, via payment intermediaries? What is the operational role of the CB and of private sector intermediaries in day-to-day payments?’

CBDC’s Pyramid Bottom Layer: Indirect or Direct Claims?

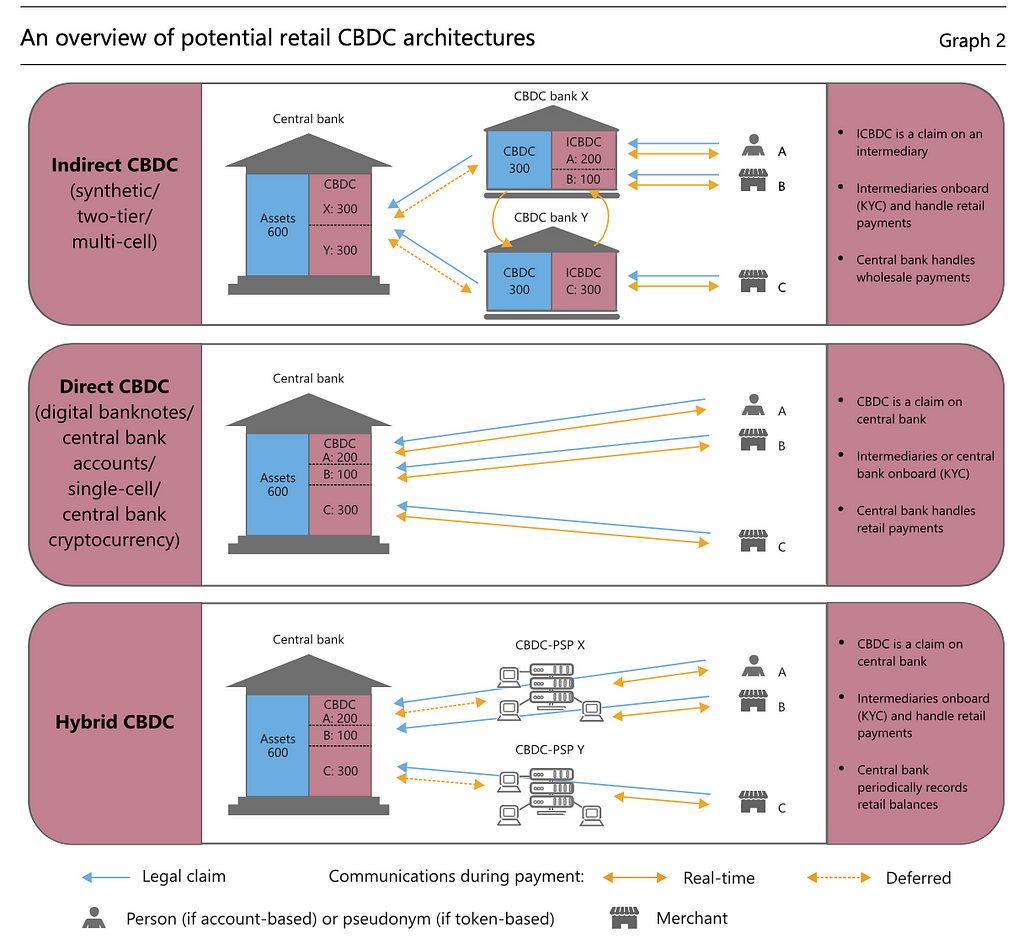

We must deem the nature of the CB which becomes the only entity issuing and redeeming these digital currencies. Furthermore, technical architectures of CBDC, presented in Figure II below, may also turn around whether we are dealing with either account- or token-based currencies, which may require different operational infrastructures.

- The “Synthetic CBDC” or “Indirect CBDC”

The first CBDC model, referred to as “synthetic CBDC” (Adrian and Mancini- Griffoli, 2019) or “indirect CBDC”, represents, as indicated by its name, consumers’ indirect claim on the CB. A third-party, serving as the intermediary (labelled as “CBDC bank” in the model) promises to back each indirect CBDC (labelled as ICBDC) to retail consumers (households and firms) via its actual holdings of fiat money — which could be CBDCs or any other type of legal tender money — deposited in CB’s accounts.

It is by this channel of intermediaries where CBs would give up part of their dominance of the system and externalise their services, thereby providing partial anonymity (which is one of the main households’ preferences, as already mentioned). However, this may trigger crucial costs for CBs since they would no longer hold whole control on the record of financial transactions, i.e. individual claims — they would only record wholesale holdings.

2. The “Direct CBDC”: Simplicity at the Cost of Anonymity

On the other hand, the elimination of dependence of third-parties may discourage consumers from using a cash-like CBDC since it would lack anonymity. Under a CBDC directly operated by a CB, accounts would be entirely managed by this institution, becoming hitherto the only handling institution.

Voices from the private sector remind Central Banks of the low experience in know-your-consumer (KYC) services and, therefore, highlight their main stance of the infeasibility of a CBDC system primarily and solely orchestrated by Central Banks.

In this scenario, a third type of legal claim comes into play: a “hybrid CBDC”.

3. “Hybrid CBDC”: The Optimal Decision?

In this case, a CBDC would still be deemed as a claim on the Central Bank but there would also exist intermediaries which would hold partial influence on the legal claim. These Payments Service Providers (PSP)would, however, be indirectly ‘governed’ by CBs; if a PSP to fails, the Central Bank chooses another functional PSP, moving the claims in bulks from the failing ones to the new ones.

Overall Conclusion On The Three Types of Claims

Central Banks being the only issuers of CBDCs would have the ultimate decision to choose the optimal design of the CBDC, taking into account their constrained maximisation problem — that is, to maximise the welfare state under the constraints regarding households’ heterogenous preferences for anonymity and security when using the payments instruments.

Direct CBDCs may appear to be really secure (note that this would depend on whether we deal with account- or token-based CBDCs) but would lack anonymity in payments. It is true that Central Banks could give up part of their control on the traceability by issuing an indirect CBDC, but at the cost of loosing trace of the electronic transactions which may give rise to wrongdoing.

Besides this, despite hybrid CBDCs may look highly promising, one of the main drawbacks for this type of individual claims is the complexity of the whole system considering Central Banks as the main issuers along with intermediaries. This may exacerbate two of the core foundational values of a CBDC, stated in the ‘CBDC Pyramid’: the easiness of use and resilience in operations.

The design and architecture of a CBDC is a current research topic and further research on the matter may help to assess the actual feasibility of a centralised digital currency. Other functionality aspects may also depend on whether the CBDC is interest-bearing and to what extent it will resemble to conventional physical cash or to bank deposits. Either extremes might threaten variety in payment instruments and, hence, a sustainable payments system; countries adopting cash-like CBDCs can reduce the demand for cash to a point where cash disappears due to powerful network effects — as it is now happening in Sweden, whereas deposit-like CBDCs could lead to an increase in deposit and loan rates, triggering a shrinkage in bank lending to households and firms. However, Central Banks could avoid this by changing interest rates were they to issue an interest-bearing CBDC. This is another research aspect which I may endeavour in an upcoming article.

References

(Auer R., Böhme R., 2020) “The technology of retail central bank digital currency”. BIS Quarterly Review, March 2020

Popper N. and Li C. (March 1 2021) “China Charges Ahead With a National Digital Currency”. The New York Times.

My Short Take On The Legal Structure Behind a ‘Retail’ CBDC was originally published in Level Up Coding on Medium, where people are continuing the conversation by highlighting and responding to this story.

This content originally appeared on Level Up Coding - Medium and was authored by Marc Clotet

Marc Clotet | Sciencx (2021-04-20T02:07:08+00:00) My Short Take On The Legal Structure Behind a ‘Retail’ CBDC. Retrieved from https://www.scien.cx/2021/04/20/my-short-take-on-the-legal-structure-behind-a-retail-cbdc/

Please log in to upload a file.

There are no updates yet.

Click the Upload button above to add an update.